Early Pandemic Construction Prices Vs. Today

by Stewart Elliott, RHC founder

How did we get here?A simple background observation

Even before the coronavirus pandemic upended the world, our country already had a housing inventory problem. Years of increasing extreme storms, more intense hurricanes and tornadoes, floods, and expanding forest fires have all devastated our landscape and thousands of homes, all required replacement. Including rebuilding entire towns in several cases. Add to this the ‘normal’ replacement housing stock of 300,000 for unsound buildings, about 700,000 homes to accommodate population growth, and the large 2nd home market of 100,000 homes; adding up to the need for over 1 million new homes annually!

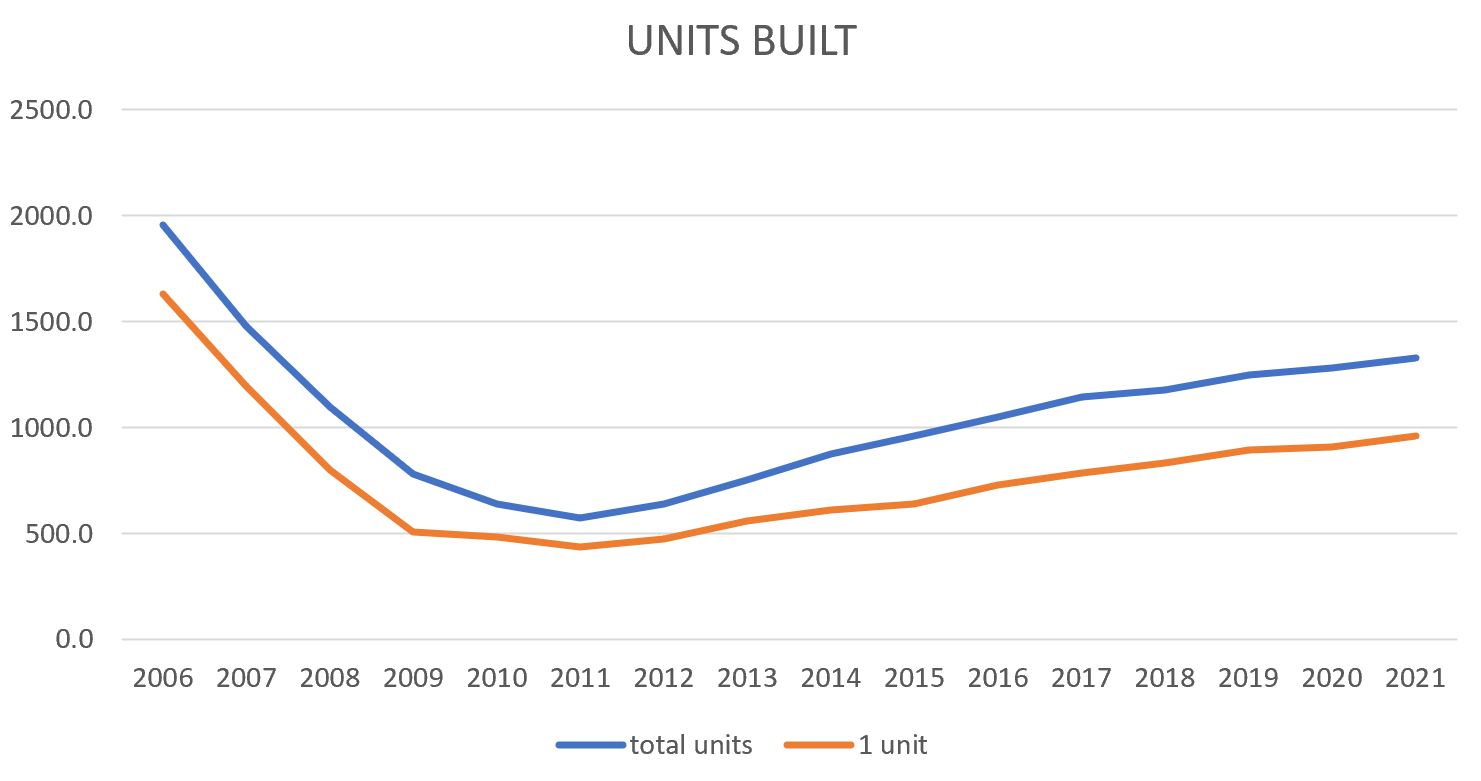

Considering the massive plunge in construction during the Great Recession of 2007 – 2009 when home construction was down to ~450,000 homes annually. The next 15 yrs. was plagued by a constantly ‘recovering’ industry, reduced workforce, and reduced qualified suppliers. The increasing disasters did not stop, and the deficit in housing continued to grow. As of 2022, the industry has yet to catch up.

In 2020, the pandemic became the major cause of housing stock reduction. Isolation and quarantines became the way of life resulting in shutting much of the industry down for a year. Suppliers and manufacturers drastically cut inventory, shut plants, laid off staff to survive.

Add global manufacturing of appliances, cabinetry, hardware, fixtures, fasteners, steel, lumber and more, and the construction industry becomes sensitive to the world economy. The reduced workforce put further pressure on the supply by reducing drivers and delivery, increasing backlog and back orders. I think it is fair to say the economy continues to be broken early in 2022 by no fault of anyone or anything – simply a perfect storm – all the factors aligned – the definition of chaos.

Our building industry estimates the current housing deficit stands at about 3 million homes as of 2021. To get back to normal, builders would need to put up about 1.4 million single-family homes a year for the next 10 yrs. We are nowhere near this as we begin 2022.

What does a typical, classically healthy housing market (real estate and construction) look like? There usually is a healthy ‘negotiations’ of price and cost for homes, both in new construction and existing homes. In a perfect real estate world, home prices would rise at the same pace as wages. While unemployment is at record lows and there are offerings of bonuses and incentives to get the workforce back, the fact is there still are not enough workers to fill the demand today and wages do not meet the present costs.

Recently (end of 2021 beginning of 2022) buying a home was a bidding war which raised prices substantially. Building a new home cost 20%-30% more; adding $30,000 in construction cost. Land prices have doubled.

While people wanted to buy goods and services and go out to eat during 2021, much of it was not available due to the shortages. Spending money continued to be difficult, so consumers saved their money. Low interest rates for savings caused many people to put their money into the stock market allowing it to grow substantially.

And we all know where this went by the end of 2021 – low interest rates, high demand, lots of available money compounded by aging equipment, no inventory, smaller workforce, and closed facilities resulted in market driven cost increases across the board. Is it any wonder there is an enormous problem with single family home availability?